Address

Hyderabad

Work Hours

Monday to Friday: 7AM - 7PM

Weekend: 10AM - 5PM

An option is a financial contract that gives the buyer the right, but not the obligation, to buy or sell an asset at a predetermined price within a specified time.

At its core, an option is a risk-transfer agreement under uncertainty. One party wants protection or asymmetric upside. Another party is willing to absorb that risk in exchange for money (premium). Options exist because the future is uncertain and different participants want different payoff structures.

Options allow investors to redesign how they experience risk and reward. But as Warren Buffett famously warned, derivatives can also become ‘financial weapons of mass destruction’ when used improperly.

There are two types of Options:

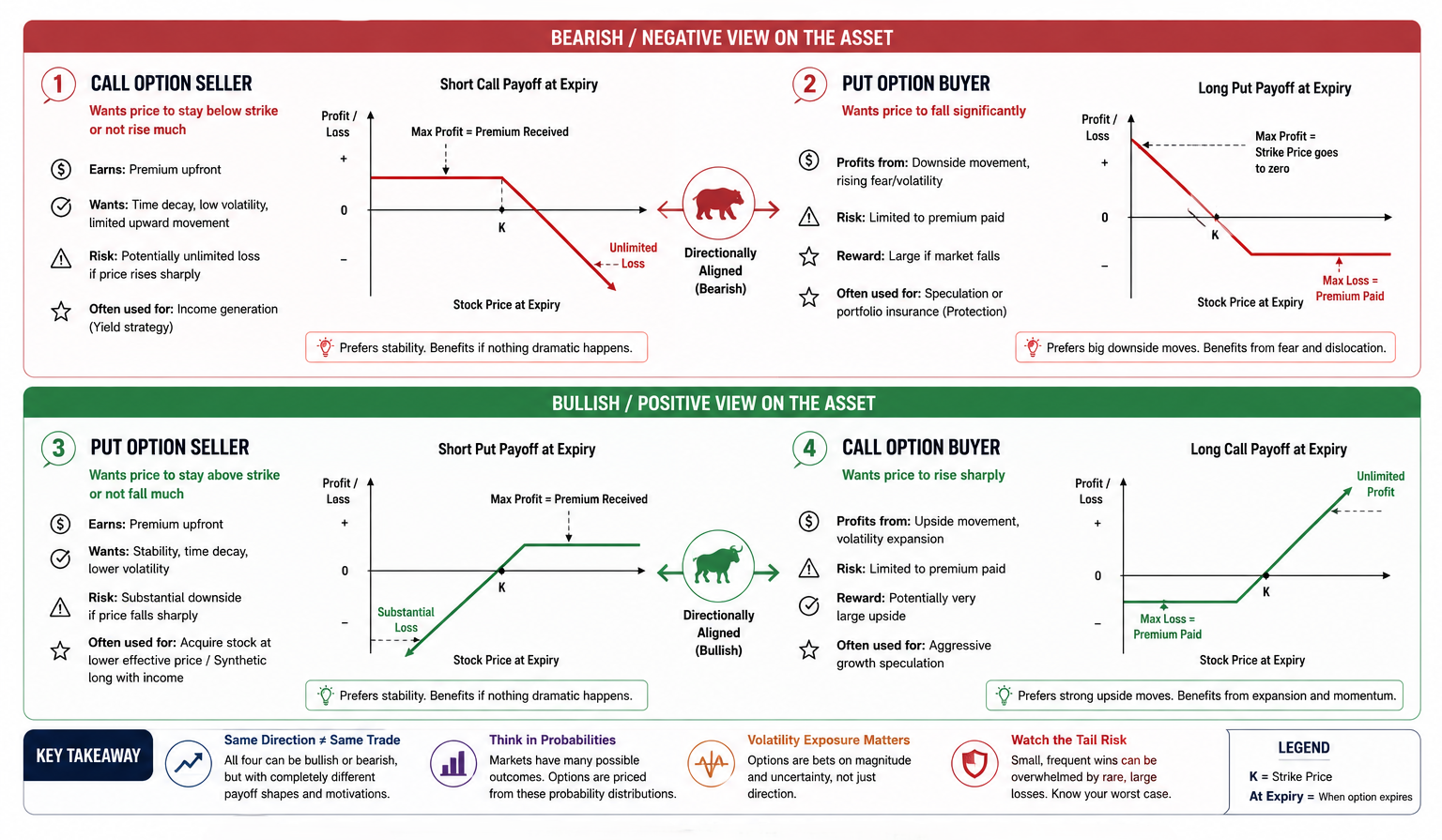

The four foundational option positions

This infographic shows the four foundational option positions that form the building blocks of all options strategies. It explains how each position participates in market upside, downside, income generation, volatility, and risk through their unique payoff structures. Every options strategy from covered calls to iron condors is built using these four foundational positions.

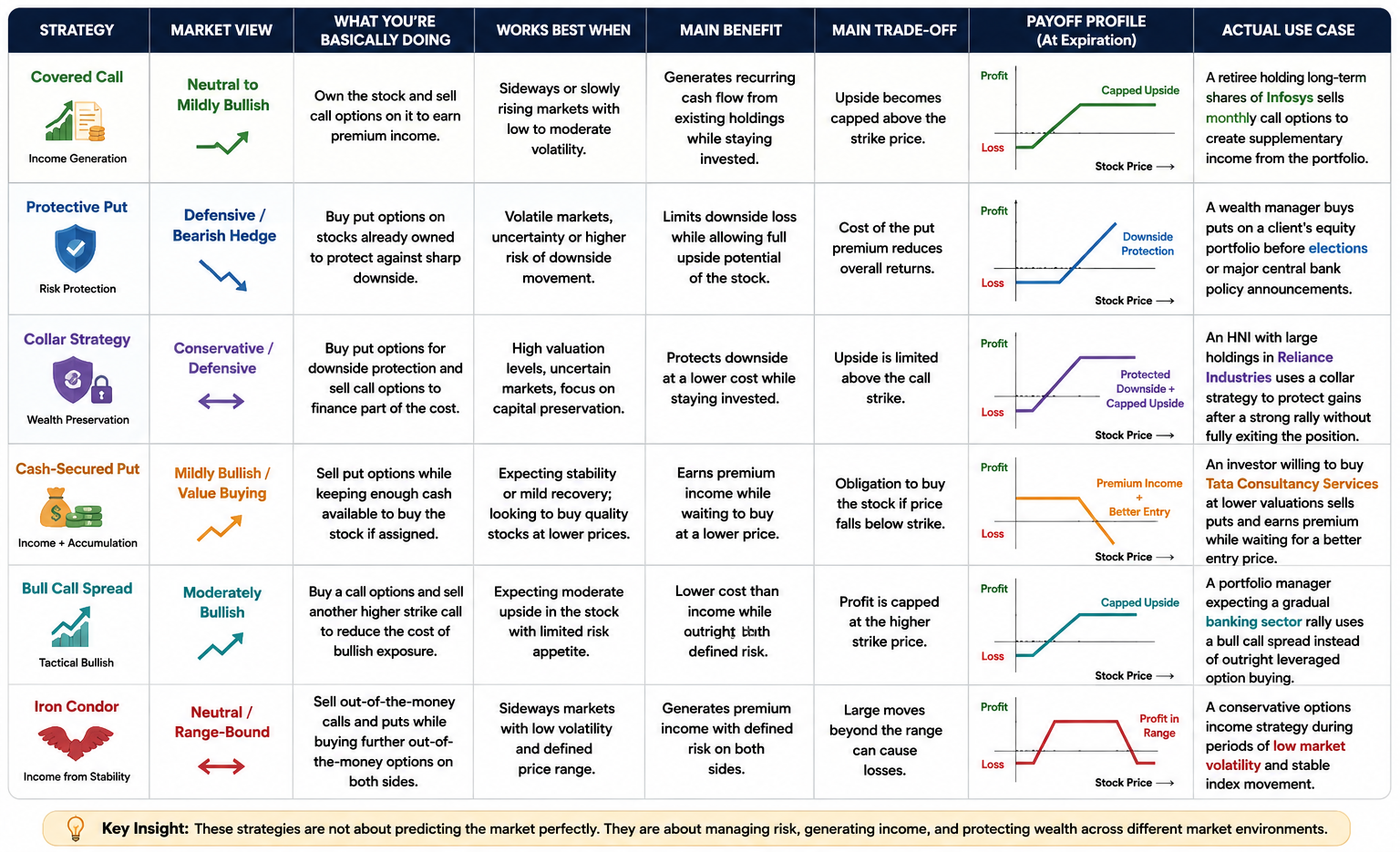

Structured Options Strategies

These are combinations of the four foundational option positions buying and selling calls and puts designed to create specific risk-

reward outcomes based on an investor’s market view, income objective, volatility expectation, or risk management need.

This table summarizes common structured options strategies, their market outlook, practical use, ideal conditions, benefits, and trade-offs in managing risk, income, direction, and volatility

| Strategy | Market View | What the Strategy Does | Works Best When | Main Benefit | Main Trade-off |

|---|---|---|---|---|---|

| Long Call | Bullish | Paying a small premium for potentially large upside exposure | Expecting strong upward movement | Limited downside, large upside potential | Time decay if stock does not move enough |

| Long Put | Bearish / Defensive | Paying for downside protection or betting on decline | Expecting market weakness or uncertainty | Protects against falling prices | Premium can expire worthless |

| Bull Call Spread | Moderately Bullish | Reducing bullish trade cost by giving up some upside | Expecting moderate upward movement | Lower premium cost | Profit becomes capped |

| Bear Put Spread | Moderately Bearish | Reducing bearish hedge cost by limiting profit range | Expecting controlled downside | Cheaper than naked puts | Limited maximum gains |

| Straddle | High Volatility | Buying both upside and downside exposure simultaneously | Expecting major movement but uncertain direction | Profits from sharp movement either way | Expensive if market stays calm |

| Strangle | High Volatility | Buying cheaper out-of-money volatility exposure | Expecting extreme movement | Lower cost than straddle | Needs bigger move to profit |

| Iron Condor | Neutral / Range-Bound | Selling volatility and betting market stays stable | Sideways, low-volatility markets | Consistent premium income | Sharp moves can create losses |

| Covered Call | Neutral to Mildly Bullish | Owning stock and renting out upside for income | Sideways or slowly rising markets | Generates recurring cash flow | Upside becomes limited |

| Protective Put | Defensive | Buying insurance on portfolio holdings | Elevated uncertainty or downside risk | Limits major losses while staying invested | Insurance cost reduces returns |

| Collar Strategy | Conservative / Defensive | Protecting downside while financing hedge cost by sacrificing some upside | Capital preservation situations | Controlled risk at lower hedging cost | Caps strong upside participation |

| Cash-Secured Put | Mildly Bullish / Value Buying | Getting paid while waiting to buy stocks cheaper | Long-term accumulation strategy | Premium income plus better entry price | Forced buying during sharp decline |

Role of Options in Wealth Management

In wealth management, options are used less for speculation and more for risk management, income generation, and portfolio stability.

Their value mainly comes from these four areas

Options Strategies for Wealth Management

This infographic explains some of the most used options strategies in wealth management, showing how investors use structured option positions to generate income, protect portfolios, preserve capital, and manage risk across different market conditions.

Case Studies – How Options Are Used in Real Markets

NVIDIA: How the Options Market Helped Shape NVIDIA’s Price Action

Historically, options were a secondary market used primarily to hedge the risk of holding the underlying stock. In the case of heavily traded mega caps like NVIDIA, the derivatives market has evolved into the primary driver of the stock’s price action. The options market is no longer just reacting to the equity; it is actively dictating it.

Sensex 30: How Index Options Influence the Market

In India, options trading is concentrated mainly in index derivatives like the NIFTY 50, BSE SENSEX, and Bank Nifty, meaning derivative flows influence the broader market first and individual stocks second.

India’s derivatives market is dominated by index options trading. As traders aggressively buy and sell index contracts, market makers hedge their exposure by trading index futures and heavyweight stocks within the Sensex. This causes derivative flows at the index level to influence the price action of the underlying stocks themselves.

Because the Sensex is weighted heavily toward large companies like HDFC Bank, Reliance Industries, ICICI Bank, and Infosys, dealers often buy or sell these stocks mechanically to hedge index options exposure. As a result, short-term price movement can become driven more by derivatives positioning than by company fundamentals.

The rise of weekly index expiry contracts has created highly concentrated short-term volatility. On expiry days, large option sellers often attempt to keep the index near heavily traded strike prices so options expire worthless, creating sharp intraday moves and artificial price swings in Sensex stocks.

A decade ago, Indian markets were driven more by cash-market investing. Today, large-cap indices are deeply influenced by derivatives activity, dealer hedging, and algorithmic flows. This creates a structural shift where large-cap price behaviour increasingly reflects options market mechanics rather than purely fundamental investing flows.

ESOPs: How Options Derivatives Shape Employee Wealth and Corporate Incentives

Employee Stock Ownership Plans (ESOPs) function similarly to call options, giving employees the right to purchase company shares at a fixed price after a vesting period. Companies use this structure to align employee incentives with long-term shareholder value creation.

GameStop: When Options Markets Overpowered Fundamentals

While NVIDIA demonstrates how options drive a massive, highly liquid mega-cap, GameStop illustrates what happens when derivative flows target an illiquid, heavily shorted small-cap equity. It perfectly encapsulates how retail capital can exploit structural vulnerabilities in institutional risk models.

GameStop was uniquely combustible because it experienced two simultaneous, overlapping squeezes:

The continuous feedback loop—retail buying calls, dealers buying shares to hedge, the price rising, shorts covering, the price rising further, forcing dealers to buy more shares—resulted in an exponential, parabolic price explosion.

Common Retail Misunderstandings About Options

Final Thoughts on Options and Derivatives

Derivatives are not merely speculative instruments. When integrated thoughtfully into a long-term portfolio, they can become tools for income generation, risk management, capital preservation, and portfolio engineering. But in financial markets, every additional return comes from accepting a different form of risk, limitation, or trade-off. Understanding that exchange is what separates strategic use from speculation.

Disclaimer: The content presented in this blog is for educational and informational purposes only and should not be considered investment advice. Options trading carries significant risk, including the potential loss of capital. Always perform your own due diligence and consult a qualified financial professional before making investment decisions.